Some thoughts on Tax Incremental Financing

The city invests tens of millions of dollars in Tax Incremental Districts. What is it for?

[Note: I will be out of town next week for work, and there will be no newsletters. I’ll return on October 10.]

Last week, the Common Council approved multiple items related to Tax Incremental Financing (TIF) and Tax Incremental Districts (TIDs)1.

These included an amendment to TID No. 10—a piece of property near the Mayfair Mall that had previously been a car dealership and is now the site of several hundred apartments—that allowed it to assume a $6 million liability to pay for the acquisition of a former Boston Department store a half mile away, and the creation of TID No. 14—encompassing several contiguous properties on W. North Avenue that will eventually contain apartments, townhomes, and commercial space—that the city is subsidizing with another $6.5 million.

These are large sums of money, and my sense after listening to dozens of these types of meetings and talking to various alders is that people tend to occupy one of three groups: (1) some, often employees of the city, believe TIDs are vital for the city’s economic development and tax base, (2) some, notably Nancy Welch when she was an alderwoman and Ald. Makhlouf right now, are very skeptical but tend to articulate this skepticism in vague ways that are sometimes factually incorrect and that people in group (1) tend to dismiss, and (3) everyone else, which includes most of the public, who find the idea confusing if they’ve even heard of it at all.

My claim is that TIDs, while potentially very useful, often seem opaque, and I wish the city had a more transparent framework for evaluating their success, because they can potentially distort incentives and development in ways that are inefficient and difficult to see. That said, they’re worth trying to understand since they cost residents and taxpayers money when they go poorly and sometimes even when they don’t.

What makes a city buy an abandoned department store?

Previously, I mentioned an amendment to the TID No. 10 project plan to help the city finance its recent purchase of the old Boston store property:

TID No. 10 was created in 2015 to help turn an abandoned car dealership into several hundred apartments near the Mayfair Mall. More recently, the city’s Community Development Authority (CDA) purchased the old Boston store less than half a mile from TID 10 for $4.1 million dollars. Two resolutions that came before the Common Council on Tuesday were related to this purchase.

The first amended the terms of the Project Plan for TID 10 so that the city was allowed to finance a loan for its recent purchase of the Boston store property with revenues from TID 10, and the second authorized the city to actually take out the $6 million loan itself. This loan would be used to pay back the CDA.

Originally introduced in 1975 as a way for local governments to restore and revitalize blighted areas in their communities, Tax Incremental Financing is a way to encourage development that the city believes would be beneficial to the community but that does not provide enough private benefit to a developer or property-owner to undertake.

This was the basis for Ald. Makhlouf’s statement last week during the Common Council meeting that “a TIF is supposed to be used for areas that are blighted. Are we really saying that the parking structures and parking lot at [the Boston store property] is a blighted area?”

But while it was originally meant for blighted areas, the law has expanded over time to allows TIFs for things like2 Environmental Remediation or industrial and mixed-use development. Even the term “blighted” isn’t particularly well-defined.

On the one hand, there is a natural incentive for the city not to create TIDs since it involves them spending money for development when the vast majority of development happens “for free.”

On the other hand, their increasing popularity is partly a function of levy limits that make it hard for municipalities in Wisconsin to raise property taxes. I described some of the history behind state levy limits in July’s “Budget gaps in Wauwatosa's finances”:

So, after a period from 1998 through 2005 when property tax levies increased annually at a rate of 5.2% despite inflation only running at 2.2%, legislators finally passed a law that said local governments could only increase the property tax level by the greater of net new construction or some variable "floor" which ranged from 2-3.86%. In 2011, the “floor” was eliminated entirely, and cities could only raise property tax if the amount of taxable property increased.

With the ability to increase revenue limited by the amount of new construction and with Wauwatosa’s own budget nearing the levy limit, the city has an incentive to encourage development that increases the value of land that they can tax. The most popular way to do that is by paying for infrastructure improvements and subsidizing development through the creation of TIDs.

How do they work?

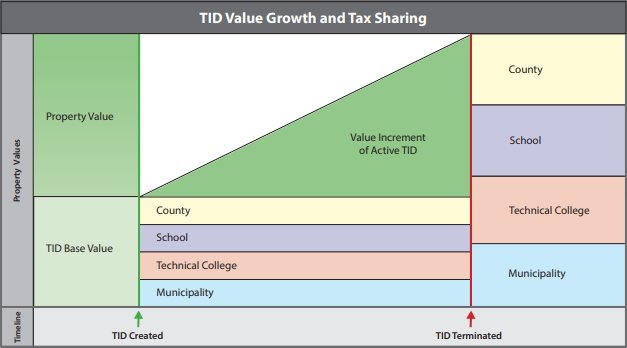

Normally, a property owner receives a tax bill based on the assessed value of their property. This tax bill does not just fund the city’s budget but budgets for Milwaukee County, the Milwaukee Metropolitan Sewer District, and the Milwaukee Area Technical college. However, the largest portion goes to the school district (about 37%) and the next largest portion goes to the city (31%).

When the city creates a TID, it freezes those taxes on the underlying properties at whatever they were before the TID was created. As development on the property progresses, it becomes more valuable and produces more tax revenue. But instead of that incremental tax revenue going to the school district, the county, the city and other “taxing authorities,” it’s used to fund infrastructure improvements—like new water mains, parking structures, or road access—within the TID or to provide a subsidy to the developer. Once the infrastructure improvements are complete or the city has paid the agreed-upon subsidy to the developer, the TID closes and that additional tax revenue now gets disbursed to all the previous taxing authorities. The city can its portion to increase its budget and reduce taxes for property owners outside the TID. As I said last week:

Designating an area as a Tax Incremental District (TID) is a way for the city to subsidize the development of newer, nicer, bigger buildings by pulling forward some of the future tax revenue they expect such a development will create and using it to entice developers to build the newer, nicer, bigger building in the first place.

For example, Wauwatosa created TID No. 2 in 1994 to develop large tracts of unused land in the Milwaukee County Research Park that would generate jobs and new businesses and diversify the region’s economy. Over an almost 20-year period, Wauwatosa provided approximately $50 million in infrastructure improvements and subsidies. By 2013, there were 14 new buildings across almost 100 acres of land with businesses employing 4,500 people. Property values over that time period increased from $4.3 million to $203 million, and this increased land value ultimately provided an additional $4.8 million in revenue to taxing authorities which was passed on to residents in the form of lower tax rates and expanded services.

While TID No. 2 closed in 2015, nine of the city’s fourteen TIDs remain open including TIDs for the UWM Innovation Campus, the Mayfair Collection, and the Village with anticipated investments from the city exceeding $55 million. A summary is available in the 2022 budget.

However, despite providing some financial information, it’s hard tell how well the TIDs have performed overall. They seem good? The 2022 budget has phrases like, “The value of the district is […] exceeding the initial projections.” And there are no “distressed TIDs”—a designation the state legislature allowed municipalities to slap onto their over-indebted, underperforming TIDs after the Great Recession cratered real estate markets. In fact, many of Wauwatosa’s are expected to pay back their loans early and close well before their maximum 27-year lifespan.

But what you’d really want to know is how much money, in total, the city has spent since the TID was created. And how much in incremental tax revenue is being produced. State law requires municipalities to file yearly reports, so I assume this information exists somewhere. It’s just not in the city’s budget. Or the city’s TIF webpage.

And what you’d really, really want to know is what development might have occurred and how valuable those properties might have become without the city’s investment at all.

What would have happened if we didn’t give developers TIF money?

The law allows municipalities to use Tax Incremental Financing (TIF) to encourage development that “would not occur but for the use of TIF.” This is, appropriately, known as the “but for” requirement.

But it’s not actually possible to know for certain whether development would have occurred without a subsidy. This is because as soon as the city provides a subsidy, we never get to witness the world where they didn’t. This might seem obvious, but the problem of making a decision and never knowing what would have happened had you decided differently is so common and difficult to overcome, it even has a name and entire textbooks devoted to teaching people how to deal with it (and flowcharts to help you decide which textbooks to read).

And arguments between those opposed to subsidizing private development and those who consider it necessary often involve quibbling about what would happen without those subsidies. One person says, “The developer won’t build without a subsidy because it’s not profitable enough,” and the other person says, “Well of course they’d say that. They want a subsidy!” And the first person comes back and says, “No, we did some projections. It’s true. They can’t profitably build this office park that we want,” and the second person says, “Well, maybe you should let them build something that is profitable.”

And occasionally the first person finally convinces the city that the only way they’ll get an office park is to pitch in several million dollars to get some company to build it only to have a different company come in a few years later and build an even larger office park right across the street without any subsidies.3

Fortunately or unfortunately, determining whether you’ve met the “but for” requirement is generally more ambiguous, and in practice the city mostly seems to prove it by (1) noticing that a property has been sitting vacant for several years with no attempt by anyone to buy it and (2) then hiring a consultant to perform financial projections and market research to determine how much they’d need to offer a developer to make the return on investment (ROI) worthwhile for them.

This at least appears to be the case for TID No. 14 on W. North Avenue (pg. 81). The city would like AbleLight and the Luther Group to provide below-market rate apartments but this will make the project too unprofitable. So the city hires a consultant to determine how much they would need to offer to make the ROI acceptable. This amounts to $6,500,000 in subsidies, interests payments, administrative costs, and improvements to streets, water utilities, and landscaping. In return, when the TID closes in 2044, the city expects the underlying property to be $15 million more valuable and generate $400,000 of additional tax revenue.

The projections are useful, but it would be nice if there was some type of transparent framework for evaluating these TIDs after they’re completed. Not just before they’re created (which already seems to exist). Do they end up meeting the projections made when the TID was approved? Were there unanticipated costs? How many jobs did they project would be created and how much did we end up with? Do they improve economic growth not just in comparison to growth rates before the TID but compared to growth rates in the rest of the city? What was the overall return on investment?

It would also be nice if the city had some agreed upon definition for “blight” or what constitutes adequate proof in meeting the “but for” requirement. I’m not aware that any of these things exists. And it certainly seems as if some of the alders are confused about this as well.

Because there are downsides and subtle ways for things to go wrong.

1.

Some of them are straightforward. For instance, some point out that freezing property taxes for the 20+ years that a TID is normally open slowly starves tax authorities of revenue as it gets eaten instead by inflation. Ten thousand dollars in 2015 is worth much than $10,000 in 2022 or 2040.

Or they point out that locking away the incremental tax revenue inside a TID for multiple decades keeps it from being used for broader city services like police or fire departments that, while they are not receiving the extra tax revenue from the newly developed TID, must still potentially expend resources responding to crimes or fires inside it. Or, if a TID is used to develop hundreds or thousands of new apartments, the parents and school-age kids that move there will require the school district to expend additional resources that aren’t offset by increased tax revenue.

And obviously, municipalities can do stupid things like overpay for properties, subsidize unviable development projects or subsidize viable ones managed by unviable businesses.

But some problems are more insidious.

2.

One of the benefits frequently cited by supporters is that TIDs not only increase property values but spur economic development—new businesses are formed, employees are hired, new stores draw more customers who spend money. But instead of increasing overall investment, a TID might simply shift investment from other parts of the city into the TID itself as developers respond to incentives. So while the TID in isolation might seem successful—development is occurring and property values are increasing—it’s just development and the creation of new businesses and the hiring of new employees that, absent the incentive, would have occurred somewhere else in the city.

Even worse, it might cause a misallocation of capital that lowers rather than raises overall growth within the city. While many studies do find that property values within a TID increase more quickly, one study by Merriman and Dye (2000) using data in metropolitan Chicago found that economic growth around TIF areas was actually lower than non-TIF areas. They suggest as a potential explanation for this fact that “government subsidies reallocate property improvements in such a way that capital is less productive in its new location,” and conclude:

[T]e empirical evidence suggests that TIF adoption has a real cost for municipal growth rates. Municipalities that elect to adopt TIF stimulate the growth of blighted areas at the expense of the larger town. We doubt that most municipal decision-makers are aware of this tradeoff or that they would willingly sacrifice significant municipal growth to create TIF districts.

Similar results are found in Dye and Merriman (2003) and Weber, Batta, and Merriman (2007) where they notice that the appreciation of commercial and industrial property within TIFs is often offset by reduced property values in nearby residential areas due to traffic congestion and other factors.

3.

One could also imagine this investment shifting problem on a regional scale. Business owners care about their next-best options. A municipality that offers TIF assistance to distinguish itself from its neighbors and draw more development only has an advantage until his neighbors start offering TIF assistance as well. Once that happens, the municipalities in the area are in the same relative position they were in before, except now everyone is worse off because they’re all offering big subsidies to developers. If a municipality wants to distinguish itself, it must now offer even larger incentives. This creates a race to the bottom that wastes money and makes everyone poorer.

This is the effect described by Byrne (2005)—which he calls strategic competition—among municipalities around Chicago, and Mann (1999) finds that communities in Indiana are more likely to use TIFs if their neighbors are using them. This idiotic and anti-social tale from Missouri about neighboring towns competing for a Wal-Mart via TIF subsidies is another nice illustration.

A corollary to this is that it would be in the long-run best interests of municipalities in the region to coordinate with one another to only supply TIF subsidies to developers at an agreed upon rate. In other words they could form a cartel, like OPEC, to coordinate and restrict supply. The downside to cartels is that, traditionally, adherence is hard to monitor (How much oil did you say you were pumping, Iran?). Also, there’s a big incentive for members of the cartel to defect.

4.

Finally, this problem not only extends geographically but temporally too. Once the city begins offering TIF subsidies to developers, future developers learn to demand it as well. Even worse, only the developer knows how likely they are to develop a piece of property, and if they credibly threaten not to pursue development without subsidies, cities will tend to grant more and larger subsidies than they need to (See Kriz (2019)).

5.

The benefits to hiring smart, creative, industrious people to run things are almost too numerous and obvious to bother repeating. But one downside is that very smart people tend to come up with pretty complicated, clever solutions to problems that often work and make everyone better off but that occasionally blow up in everyone’s face because the thing was too complex to recognize its weaknesses.

For instance, the complexity of mortgage-backed securities often gets blamed for partially causing the Great Recession. But a better example is Enron. The book about their spectacular rise and epic destruction is even titled The Smartest Guys in the Room. The story is mostly about fraud but it’s also about a bunch of very intelligent people creating complicated energy trading markets that are supposed to make electricity provision more efficient but end up causing blackouts throughout the state of California. I can’t find the quote now, but I vaguely remember the authors saying at one point, “If you hand a bunch of enormously smart, young, competitive people a 500-page rule book and tell them to go make money, they’re going to scour that 500-page rule book and exploit every possible loop hole they can find.” For Enron’s energy traders, this apparently meant calling up power plants in Las Vegas and asking them to find reasons to shut down so they could drive up the price of electricity.

I don’t think Wauwatosa is a massive multi-billion dollar fraud waiting to collapse and cause statewide blackouts, but I do think TIFs are somewhat complex legal and financial mechanisms, and I do notice the city’s Finance Director, John Ruggini, describing TID No. 10 and the purchase of the Boston store property like this:

John Ruggini: What happened in July is that the Community Development Authority actually purchased that property. At some point in the future when we transfer that property to a developer, the TIF is going to reimburse the Community Development Authority for writing down the value of that property or selling that property for $0. In doing so, the TIF will then pay debt service—the borrowed money back—that was incurred in July.

I'll pause, because it took us probably five conference calls and countless hours and Quarles & Brady [LLP] kicking the TIF law to make sure we could do all this.

Ald. Fuerst: Who are we selling it to for $0?

John Ruggini: We don’t know yet.

I mean, it’ll probably work. It’s not that complicated. But the economy is starting to sputter a little. When recessions occur, businesses close, people are laid off, and investors are willing to take fewer risks. What if there’s no one to give the building to?

These terms get used somewhat interchangeably, but I’ll mostly use TID.

And see the TIF Manual put out by the Wisconsin Department of Revenue, particularly pages 10-14 which summarize various changes to the law over the last 45 years.

I don’t know if there’s more context to this story I’ve linked to, but as it is, it is pretty amusing.

There is always an inherent danger in believing that the future will emulate the past. "Of course property values will increase, and at a rate that mirrors what we've seen." It pays to at least model what could happen if that's not true to understand some of the risk involved.

Good article Ben. I appreciate you citing Chicago. I come from that land where almost the entire city is covered in TIFs. It is sad developers across the US expect TIF assistance if a community wants any infrastructure upgrades, affordable housing, etc.

Tosa is one of the few municipalities left in the state with a AAA bond rating which means city staff are doing something right. That said, we don't want to make the mistakes of other cities and blanket everything in TIDs.

Some additional follow-up, in the budget documents that are coming up, the performance of each TID is included. Tosa is currently has 5% of it's total value in a TIF which is less than the 12% limit by the state.